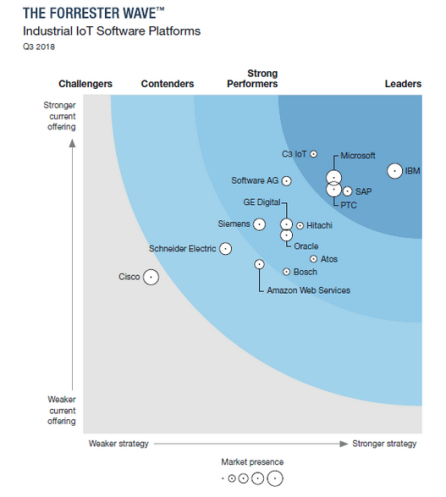

I feel 2019 will be a make or break year for the platform providers for IIoT solutions. We are getting a real sense of clarity on who is leading the pack, who is struggling to keep up and some becoming real laggards, that need to change their game dramatically to stay in the platform hunt.

I feel 2019 will be a make or break year for the platform providers for IIoT solutions. We are getting a real sense of clarity on who is leading the pack, who is struggling to keep up and some becoming real laggards, that need to change their game dramatically to stay in the platform hunt.

Clients need to come off their fence in where to invest and make some defining I(I)oT decisions. Yet to allow this to take place we need a far greater clarity of the value and real positioning of the platform providers. We need to extract the real business value understanding and ditch all the “hype” that is drowning out the real understanding. Ditch the noise, increase the signal

When you look at this top fifteen provides you can break them out between those coming from the industrial solution providers (Siemens, Schneider Electric, Bosch, GE Digital, Hitachi) and those coming from a technology conglomerate positioning (AWS, Microsoft) those that are well known for specialised offering in technology solutions (IBM, SAP, Oracle, Cisco, Atos) and those that give perhaps greater specialised IoT focus in their business model (Software AG, PTC,C3 IoT)

How do you choose between these for your own solutions?

One thing enterprises struggling with is who to go with, that committing too, longer-term. Let us not forget, it is not one, it is a selection of those platform providers that when combined will offer you solutions to a significant part of your solution need. Partly, the decisions considers does depend on which industry you are in, the type of solutions you are looking towards to solve, so as resolve your biggest problems in your digital transformation. Also, you have to consider the technology providers you have built a history with, often equally caught up in legacy issues, or those you determine will be best at managing your cloud and edge issues (management, storage, analysis, remote connections) going forward.

Software stacks. This conquers up a certain mystery for me, so I decided to order up a plate to see if I can digest all they seem to be offering.

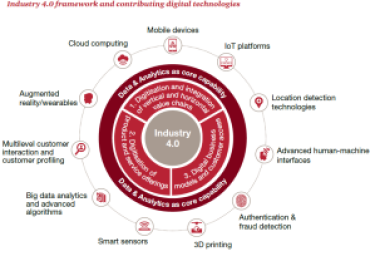

Software stacks. This conquers up a certain mystery for me, so I decided to order up a plate to see if I can digest all they seem to be offering. Ecosystems in our business thinking have suddenly become of age, they can enable cross-cutting innovation to be delivered in highly collaborative and dynamic ways. Understanding the value of working within an ecosystem is becoming critical to understand.

Ecosystems in our business thinking have suddenly become of age, they can enable cross-cutting innovation to be delivered in highly collaborative and dynamic ways. Understanding the value of working within an ecosystem is becoming critical to understand. There are twin forces at work, feeding off each other and innovation can become the greater unifier. We are facing greater disruption and an increasing innovation and technology pace. These are constantly combining, relentlessly adding a new shape to our future. We are actually caught up in a very revolutionary period.

There are twin forces at work, feeding off each other and innovation can become the greater unifier. We are facing greater disruption and an increasing innovation and technology pace. These are constantly combining, relentlessly adding a new shape to our future. We are actually caught up in a very revolutionary period. There is a new set of battlegrounds brewing around platforms and ecosystems and what and who controls the data and the flows needed to build these thriving environments, reliant on the cloud.

There is a new set of battlegrounds brewing around platforms and ecosystems and what and who controls the data and the flows needed to build these thriving environments, reliant on the cloud. So what is the difference between a fog and a cloud? Well, actually bandwidth is part of the answer and where data needs to be situated.

So what is the difference between a fog and a cloud? Well, actually bandwidth is part of the answer and where data needs to be situated. Bosch takes connected devices, open platforms, and interoperability for IoT solutions to drive your business, built from their own deployed experiences. They are focusing on knowledgeable development & deployment to provide a single integrated set of ‘connecting’ solutions.

Bosch takes connected devices, open platforms, and interoperability for IoT solutions to drive your business, built from their own deployed experiences. They are focusing on knowledgeable development & deployment to provide a single integrated set of ‘connecting’ solutions. How are organizations dealing with digital transformation and especially IoT? The key has to be one where sustainable success is central.

How are organizations dealing with digital transformation and especially IoT? The key has to be one where sustainable success is central. Paul and I have been writing mostly about ecosystems and platforms in the abstract to date, not spending a lot of time talking about specific companies or industries.

Paul and I have been writing mostly about ecosystems and platforms in the abstract to date, not spending a lot of time talking about specific companies or industries.