IIoT platforms-as-a-service are gaining ground. In my first part of a two-part post, I was raising a number of questions. That questioning continues here in part two, at a deeper level. I do recommend you read the first post to place this more into the context required.

IIoT platforms-as-a-service are gaining ground. In my first part of a two-part post, I was raising a number of questions. That questioning continues here in part two, at a deeper level. I do recommend you read the first post to place this more into the context required.

IIoT Platform providers are building new digital solutions. There are constant daily gains. A new client win here, a new contract there.

Yet the battle is one of attrition, client by client. Do you win in this approach? To gain traction, all the IIoT platform providers seem to have pressing needs to overcome massive client resistance at this present time. Platform uptake is gradual, it needs a higher depth in resolution, in the value of platforms, in their momentum. What is its value proposition to the client, the one who buys that solution? Is it still too early in their own digital transformation journey? Actually, clients are having a hard time in this and many other digital decisions.

A report recently commissioned, sponsored by GE, was researching on the emerging gaps between executive outlook for digital transformation and initiatives organizations have in place to achieve a higher uptake and engagement in platforms It was highly revealing.

Just to pick up on a couple of headline grabbers.

The GE funded report found Eighty percent (80%) believe IIoT will or could transform their companies or industry. Yet, only 8 percent yet say digital transformation is ingrained in their business and 10 percent have no digital transformation plan even in place. The reasons were varied but it seems present solutions by the platform providers are not resonating as strongly as they should be.

Honing the value proposition is a work-in-progress

Of course, we are seeing the classic list of winning stories, of the validation of the business case but these are specific, actually highly specific. They may help advance and capture new ground but they are not enough to win the new digital connected (war) argument for many or resolve their own positions. Something needs to change in the proposition of the IIoT platform BM or we have a real wait. There are alternatives but they need a different narrative to build around.

There seem lots of inhibitors to uptake by those you would expect to buy these platform services. Besides where they will invest their money, it is trustworthiness of the vendor, yes, even those who they buy their physical assets from (!) and this real fear of early lock-in where there might emerge different digital solutions.

Also, we have the growing list of concerns around implementation.

Those system/development integration costs associated with any project of this size and commitment. We have time to implement successfully and all the associated connecting up costs, the users inexperience in the technology or solutions provided, the worry or later realization that the solutions did not actually meet the business requirements, they just layered on complexity and always that lack of internal IT resources to support this, often across multiple sites of deployment to get any value of it.

The bottom line here is businesses are challenged. Can many companies actually understand cutting-edge solutions? The Aberdeen Group in association with IBM has looked at IoT issues in a recent report on this and it is showing a true “stack” of problems to work through.

There are some real worries over the true ability to truly connect all into the platform and gain returns on the investments made in the ways being described. The goal of any platform is to reduce your development risk and stay up-to-date on rapid changes in digital technology and working within a community makes powerful sense for this, accelerate your product’s time-to-market or achieving a greater productivity than today, and reduce cost in downtime, inefficient use of your assets are powerful aspects to consider and make the business case.

Blowing away many of those dark clouds

The value of dealing with the IIoT platform provider is they know your industry, the likelihood is they supplied the assets in the first place, so you have a shared interest in maximizing the assets deployed.They have firstly, their reputation on the line, they can enable you as a client to tap into the larger community, they are busy building greater functionality into the applications (ASP’s) to keep improving on solutions.

In your platform providers, you have horizontal and vertical providers, ie. choosing Microsoft Azure or Siemens Mindsphere for example. Those that are vertical solution providers do have a deep domain knowledge to help bridge numerous issues (regulations, data, and analytics) and finally, a growing solutions team that makes “on-boarding” and helping in your architecture, structures and supporting you in your proof-of-concept to realization steps. They are becoming “one-stop solution providers. They can provide a digitally constructed backbone through these IIoT platforms. Vertical providers have been realizing they have to partner with either/ and Microsoft Azure, AWS for Amazon or IBM and Watson as they, themselves, lack the bandwidth to go alone. We are seeing the “twinning or eventual winning model” emerge out of this.

Yet the dark clouds continue to stack up

The applications being built (for clients) are claimed as real solutions to their problems but are they? How deep is the domain knowledge if it is outsourced due to lack of internal resources on the vertical platform providers? I have heard a number of apps, claiming to be solutions have been far from that from one specific vertical provider as their internal software developers had actually little exposure to the business. The quality of the resource is something you need to put a “buyer beware sticker on” if this is not to continue.

What about the really massive task of re-orientating the organization into a digital reliant one. Does each company have different methodologies, of course? Legacy systems have held organizations back, resolutions are complex and expensive for many. Connecting up old machines, resolving multiple software protocols is highly specialized work. The ability to bring platform solutions inside is inhibited today, largely by a lack of digital maturity, legacy issues or alignment. This holds many back from making platform commitments. There is a massive lag as partly pointed out in the GE report.

There are actually far more issues to bridge and overcome but these mentioned above are wicked constraints, or immobilizing boards or IT to commit. There is much still needed to be overcome. Picking up on these and bridging these gaps is essential to define, understand and know if you are considering a platform solution or a provider of solutions. Are the IIoT providers taking into account the list of real concerns that are out there or just deploying all the consultants brought in on the platform to go in and solve these? The client welcomes in the trojan horse (see the previous article) and is that consultant welcomed or in conflict with their own approved list of providers of consulting services?

As you investigate IIoT platforms you see lots of similarities.

If you surround yourself with the same type of “consulting generals”, schooled in the same school of digital technology building, there is a good chance you will get much of the same result and a price. Clients are looking for a different proposition I feel. More than likely a different business model for them to invest time and understanding in, one that is committing their digital future, needs figuring out that it has a good chance of being a winning one for them. The mid-tier or specialized consultant, might offer more focused value but are they partners of choice offered on the IIoT platform? So the platform is not as open as it should be.

Being in a community, a thriving ecosystem of equal partners extracting value, made up of a very diverse set of connected parties is yet to come but we need to set the conditions, the environment for this to come into force now, not try and retrofit it later. This is one of the powerful unlocking keys for platform providers today.

Understanding Ecosystem Management is becoming critical to design into future solutions

Here lies my central theme that the real need is to deeply think through the ecosystem conditions and framework, as it has the transforming aspect missing. For all involved, this still needs a lot of work and understanding. An ecosystem is not just another buzzword, it needs framing well.

So today it is all to play for but perhaps we need new Strategic design leadership here?

Who of the current IIoT platform providers will change the game, shift the positioning and recognize the current barriers to major advancement is through a different type of digital play? Have they the time and resources to allow the majority of customers to catch up in digital maturity? Will some of those early platform providers run out of cash, patience or recognize that the specialists all inside the platform (Microsoft Azure, IBM and it’s Watson, AWS from Amazon) are better equipped to be the platform provider as the technology evolution continues with constant high investments.

We are only at the beginning of IIoT, of platforms, of digitalization, being realized by the majority. A lot is holding the majority back to make the transformation needed, for this and all things digital within their organizations.

There are big barriers to committing to specific (specialized) IIoT platforms

In summary for clients, they have critical questions to have resolved before many will commit to specific platforms. The big ones are where they will invest their money, they are questioning the trustworthiness of the vendor, even though they have invested in their physical assets, and this real fear of early lock-in, and finally as the big roadblocks, the ability to truly connect to the platform and gain returns on the investments made.

Of course, the biggest one, are you, as a client, ready for your own digital transformation? This is a deeply committing and expensive undertaking. It might initially be contained in operations or manufacturing but the true value of “going digital” is for all to be involved, to relate, to leverage and ‘mine’ the data knowledge and extract the specific value to help in your role, across the whole organization and in your partners that equally need to know and respond.

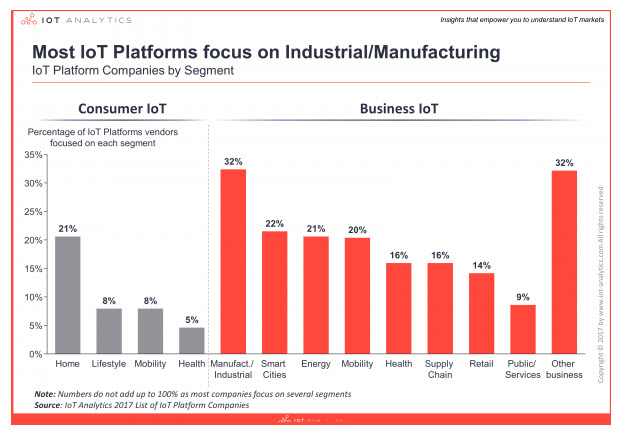

Lastly, on present count, there are over 450 platform providers, catering to both B2B and B2C. IoT Analytics produce a report listing these. If your business spans different industry sectors, how many platforms can you afford to have?

The balance in designing platforms for equitable distribution is hard.

Are the applications being built (for clients), claimed as real solutions to their problems, but are they? What about the really massive task of re-orientating the organization into a digital reliant one that goes with constant data flows? Data needs to build new value, otherwise, it simply stays a “data for data’s sake”. How can platform partners help in the supply of data? Analytics need to become more intelligent and actionable.

There are actually far more issues to bridge and overcome but these mentioned above are wicked constraints, that need to be overcome. Picking up on these and bridging these gaps is essential to know if you are considering a platform solution or a provider of solutions. Are the IIoT providers taking into account the list of real concerns that are out there?

More on another day as we keep a real focus on IIoT platform providers. Industrial domination by one or even a few is premature for any involved. All we can see it is well underway, with many twists and turns to come.

I have seen varying estimates around IoT platforms and IoT in general. The pie is huge. One example quoted this: The IoT will result in $1.7 trillion in value added to the global economy in 2019. This includes hardware, software, installation costs, management services, and economic value added from realized IoT efficiencies.

Finally, I wrote an opening article recently for www.iiot-world.com.

It was about fleshing out an opening snapshot of the world of IIoT platform providers. Go over and take a read, please.

IIoT platforms are evolving. To learn more or delve deeper I am in discussions with IIoT-World to build more about platforms understanding together, well that’s our current intent. We want to build a community offering an independent service for those that need thoughtful advice on what they need to know and understand.

Who said being an industrial giant is boring. Take note Silicon Valley; the “asset-heavy industrial muscle” is getting tuned up and the lasting potential of having industry connected up is massive in projected value.

Where are you in your IIoT platform decision journey? My aim is to help explore aspects of this journey as it is part of our connected future. These questions do have answers but they need systematically working through from the clients perspective, not the platform providers one. This is where the focus lies today for all involved.

Comments are closed.